Financing Options for Non-Residents: Local Banks vs Developer Payment Plans

When securing real estate abroad, expats want to know all their options. Purchasing a property is already challenging in one's home country, let alone abroad. Moreover, Panama has been attracting real estate buyers and investors in general. Firstly, because of its market, which is in the epicenter of major growth, and secondly, because of the residency options that come with real estate.

How hard is it to obtain a mortgage for foreigners? 2026 can be the year in which you include Panama in your plans, both through real estate and residency.

Why Non-Residents Face Unique Financing Challenges

Regulatory & Compliance Hurdles

The country naturally benefits its own, that is, citizens and foreign residents. For them, loan rates are lower and due diligence is milder. On the other hand, foreigners must be ready to present more documentation and proof regarding the source of funds, the activities, the credit status, and so on.

Currency & Cross-Border Payment Restrictions

When investing abroad, currency must always be taken into consideration. In fact, this is one of the reasons why Panama is consistently chosen by expats and investors. Since the beginning of its history, Panama has made smart decisions, one of which was to peg its currency to the US dollar.

The reality is that in everyday transactions (groceries, purchases, utility bills, restaurants, etc.) you pay with U.S. dollars, as this is the legal tender. As for the Balboa, it’s issued only in the form of coins. To sum up, in Panama you'll find dollar bills and both Balboa and dollar coins.

Undoubtedly, investing in a country with a dollarized economy helps you avoid volatility, bank runs, inflation, and exchange rates. Besides, it adds the benefit of providing an overall solid economic structure, which is what any sane investor looks for when operating abroad.

Local Bank Mortgages: How They Work for Foreign Buyers

Eligibility Requirements & Documentation

As we mentioned before, foreign residents face more red tape than locals, and the requirements in general are more demanding. The down payment for foreigners is higher, typically 30%. They are also required to submit proof of having a stable income and the capability of repayment, which can be particularly challenging for self-employed applicants.

The age restrictions are stricter, and the terms are subject to the applicant’s age. The older the applicant, the shorter the term to cover all payments. Finally, it's not unusual for banks to require life insurance with the bank as a beneficiary.

Requirements to acquire loans in Panama

- Copy of the passport (all pages)

- Second ID (National ID or driver's license)

- Proof of address (utility bill)

- CV

- Bank reference letters

- Professional or personal references

- Credit report issued in the home country and through reliable sources

- Proof of income (employment letter, payment invoices, or corporate documents)

- Two years of tax returns

- Bank statements dating back to six months or two years

- Proof of assets

- Proof of having made the deposit

- Signed purchase agreement

- Title of the property

- Recent property appraisal

- All documents must be translated into Spanish and legalized or apostilled

Disclaimer: the requirements stipulated above provide general information; however, these details must be confirmed with each bank and considering the case. All the details and information provided in this article should be confirmed through formal consultations with a certified professional. This article doesn't constitute legal advice.

How safe are banks in Panama

This amount of red tape can be discouraging, but there's always a silver lining. Another way to look at the situation is to understand how these restrictions reflect the sector's solid commitment to transparency, safety, and solidity. All banks in Panama are regulated by the Superintendency of Banks, which stipulates a robust regulatory framework for all licensed banking institutions in the country, both local and foreign.

This is yet another opportunity to see Panama as a strong player in the financial arena, not only in the region but also at an international level.

Interest Rates & Loan Tenures

Loan rates can be significantly higher for foreigners (usually 2% higher), while the down payments are more demanding. For locals, the down payment can vary from 10% to 20%, whereas foreigners can expect to pay up to 40% or 50%, and with shorter terms.

Developer Payment Plans: Structure & Flexibility

Other foreigners may prefer to opt for developer payment plans. Even though they require financial commitment, the pressure is lower as you're not putting the asset as collateral (like with a mortgage). Next, we analyze payment plans by developers, details, information, and advantages.

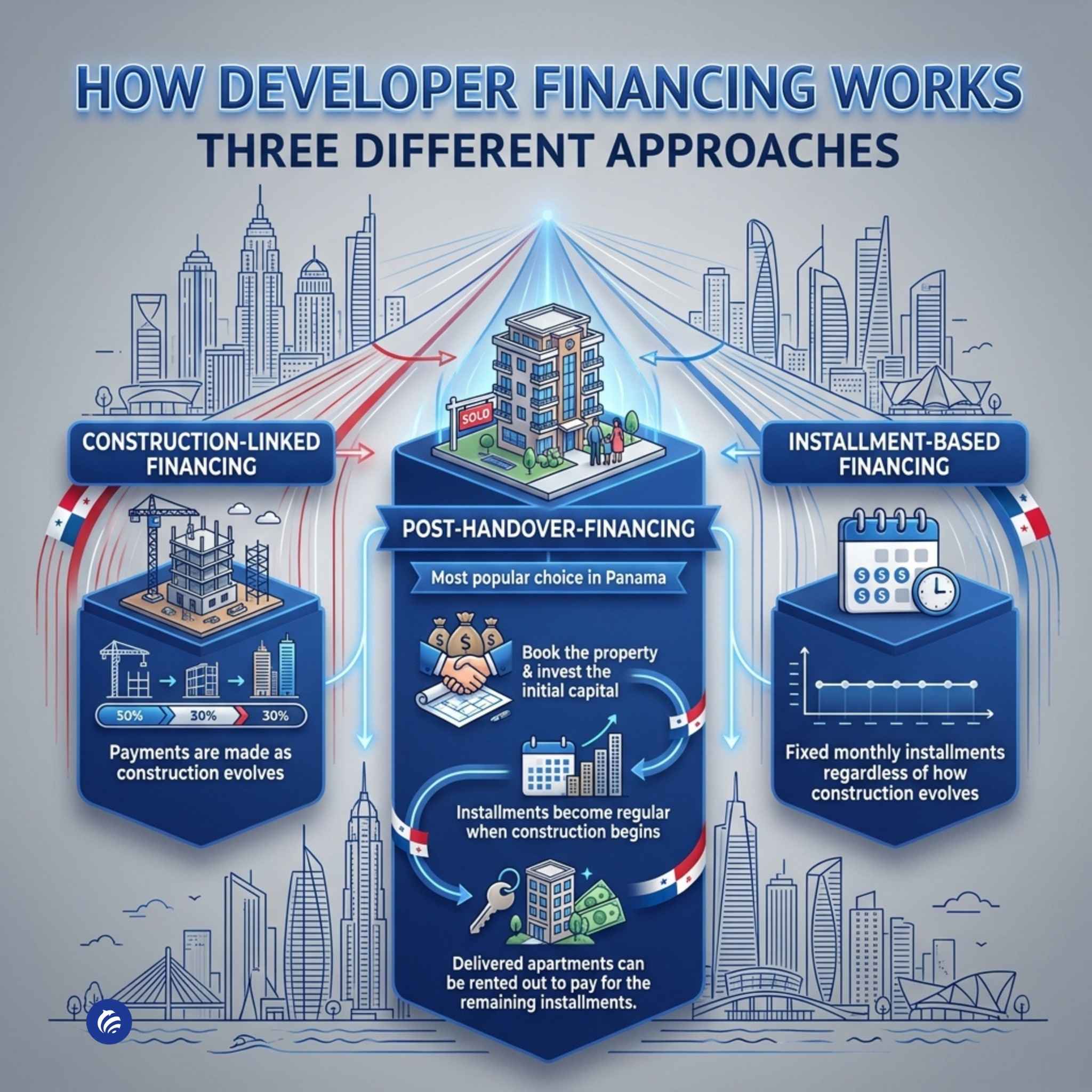

Financing plans by developers: Common Models

Construction-linked financing

This approach is mainly linked to how construction advances. With each new milestone (setting up the foundations, laying down the floor, or completing the structure), the investor must make payments to cover different percentages.

Installment-based financing

Installment-based financing is based on a payment plan through a stipulated period of time. In simpler words, the investor will have to pay a flat percentage per month regardless of how the construction develops.

Post-Handover-financing

This is the most popular choice in Panama and a perfect alternative to mortgages. Investors choose it because, once constructed, the rental income can help cover the installments.

Naturally, the buyer must invest an initial capital in the earlier phases. After booking the property, which is usually approximately $5000, the investor must continue paying and covering percentages as agreed. The initial payments are usually 5%, 10%, and 20%.

When construction starts, payments become regular, and when the building is constructed, the apartments can be rented out to cover the monthly payments. Buyers should find out in advance whether this is permitted by the complex’s rules and the local legislation.

Mundo experts' tips on buying real estate: the importance of a short-term rental license

When buying a unit through developer financing, our experts strongly suggest choosing a project that has a short-term rental license already in place. Such a license is both challenging and valuable. It’s challenging because it’s not easy to get since it requires the construction to have certain characteristics. And it is valuable because, with it, the investor can provide accommodation to the numerous people who visit Panama each year: tourists, business people, conference attendees, patients coming for medical care, temporary employees, digital nomads, and so on.

Luckily, developers are contemplating this possibility from the very inception of their projects. Many have a short-term rental license before construction begins, so they can build it according to the requirements. This is easier than making changes to an already-built structure.

Another advantage is that they are increasingly including rental management services that take the management burden off the investors’ shoulders.

Bank loans vs developer financing

Bank loans | Developer financing | |

Overall costs | Lower | Higher |

| Safety | Protected under strict regulation | Insolvency risk |

Ownership | Legal ownership right away | Title is registered once constructed |

Initial capital | Higher (from 20% to 50%) | Lower (usually 10%- 20%) |

| Payments | High financial pressure and risk of losing the collateral | Payments can be staggered due to project’s delays |

| Approval | Rigorous documentation and long approval process | Minimum documentation and easy approval |

Frequently Asked Questions

Can I obtain residency if I buy real estate through a mortgage?

Some programs, like the Friendly Nations and the Qualified Investor, allow you to use a bank loan for the qualifying property. There's an important point to make: the minimum investment must be paid up front. For the Qualified Investor, it's $300,000, while for Friendly Nations is $200,000. The remaining can be paid through a loan.

Can I obtain residency if I buy property through developer financing?

In Panama, the only program that allows this is Qualified Investor. The buyer is required to pay the $300,000 up front, and the remaining money under the terms agreed with the developer.

Can I obtain a mortgage if I'm not a resident in Panama or a Panamanian citizen?

Foreigners can ask for bank loans in Panama; nevertheless, they will be facing much stricter due diligence, higher interest rates, and more demanding down payments.

Final thoughts on buying property in Panama with a mortgage or a financing plan

A mortgage, a bank loan, or a financing plan can be the answer for investors who don't have the full cash or those who prefer a different approach.

In our view, developer financing is ideal for those building a real estate portfolio that ends up paying for itself. The risk of insolvency, failure to deliver, or failure to deliver according to the agreed-upon terms, is always lurking. Therefore, it’s better to look for developers with a verifiable history.

The mortgage, on the other hand, allows you to use the property right away, with the downside of having your property as collateral and risking it if you ever face financial hardship. With loans lasting 10 or 20 years, not everyone is willing to take that chance. Developer plans tend to be more flexible, and you only risk what you have already invested, not an asset or your entire savings.

Who we are

Mundo, as master brokers for Mercan group projects, have ample connections with developers across Panama. Some of our partners have built several buildings in Panama City, and these constructions are proof of their credibility and commitment to quality.

We can help you choose a real estate property and obtain residency with a single move, leveraging the straightforward Panama residency programs.

We are a consolidated team of experts, lawyers, realtors, and advisors specializing in corporate, banking, real estate, and economic migration. Browse our site or contact us to know the jurisdictions we operate in: Sao Tome, Vanuatu, the Caribbean, the UK, the US, Seychelles, Singapore, Hong Kong, Nevis, and many others. Get in touch now and let's make your objectives a reality.

.png.small.WebP)

.webp.small.WebP)

$347,000

$309,100

$300,000

$250,000

$424,000

Many of our readers are concerned about the risk of buying property abroad. Any foreigner embarking ...

Panama enjoys a rare combination of factors that contribute to making it a real estate hub in the re...

When there's a new program in the CBI world, everyone talks about it. Comparisons are common between...

Today, we go back to analyzing the new African CBI program, which has been on the lips of experts an...

The migration world has been increasingly tied to finances since wealthy people started to choose sm...

The financial world is facing dramatic changes, and structures need to be ready to accompany clients...